Load Data

file = system.file("extdata", "USeconomic.csv", package = "tswgewrapped", mustWork = TRUE)

data = read.csv(file, header = TRUE, stringsAsFactors = FALSE, check.names = FALSE)

names(data) = gsub("[(|)]", "", colnames(data))

Get Model Recommendations

lag.max = 10

models = list("AIC None" = list(select = "aic", trend_type = "none", lag.max = lag.max),

"AIC Trend" = list(select = "aic", trend_type = "trend", lag.max = lag.max),

"AIC Both" = list(select = "aic", trend_type = "both", lag.max = lag.max),

"BIC None" = list(select = "bic", trend_type = "none", lag.max = lag.max),

"BIC Trend" = list(select = "bic", trend_type = "trend", lag.max = lag.max),

"BIC Both" = list(select = "bic", trend_type = "both", lag.max = lag.max))

var_interest = 'logGNP'mdl_build = ModelBuildMultivariateVAR$new(data = data, var_interest = var_interest,

mdl_list = models, verbose = 1)

#>

#> Model: AIC None

#> Trend type: none

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.979949e+01 -4.043610e+01 -4.049031e+01 -4.041841e+01

#> HQ(n) -3.965317e+01 -4.014345e+01 -4.005134e+01 -3.983312e+01

#> SC(n) -3.943933e+01 -3.971577e+01 -3.940982e+01 -3.897776e+01

#> FPE(n) 5.192033e-18 2.748673e-18 2.607880e-18 2.811272e-18

#> 5 6 7 8

#> AIC(n) -4.037845e+01 -4.041713e+01 -4.032619e+01 -4.034898e+01

#> HQ(n) -3.964684e+01 -3.953920e+01 -3.930193e+01 -3.917840e+01

#> SC(n) -3.857764e+01 -3.825616e+01 -3.780505e+01 -3.746768e+01

#> FPE(n) 2.941472e-18 2.852623e-18 3.159796e-18 3.136181e-18

#> 9 10

#> AIC(n) -4.033399e+01 -4.037318e+01

#> HQ(n) -3.901708e+01 -3.890995e+01

#> SC(n) -3.709252e+01 -3.677155e+01

#> FPE(n) 3.247802e-18 3.203453e-18

#>

#>

#> Lag K to use for the VAR Model: 3

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0227911 -0.0059353 0.0008095 0.0056885 0.0214455

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 0.026269 0.114301 0.230 0.8186

#> logGNP.l1 1.057405 0.098851 10.697 <2e-16 ***

#> rs.l1 -0.224098 0.134021 -1.672 0.0971 .

#> rl.l1 0.491966 0.274355 1.793 0.0754 .

#> logM1.l2 0.070436 0.175106 0.402 0.6882

#> logGNP.l2 0.009095 0.133053 0.068 0.9456

#> rs.l2 -0.149187 0.186274 -0.801 0.4248

#> rl.l2 -0.434827 0.385994 -1.127 0.2622

#> logM1.l3 -0.117121 0.095870 -1.222 0.2242

#> logGNP.l3 -0.047856 0.092147 -0.519 0.6045

#> rs.l3 0.081275 0.148235 0.548 0.5845

#> rl.l3 0.014681 0.296199 0.050 0.9606

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008783 on 121 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 8.734e+06 on 12 and 121 DF, p-value: < 2.2e-16

#>

#>

#> Model: AIC Trend

#> Trend type: trend

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.976174e+01 -4.044348e+01 -4.049058e+01 -4.041902e+01

#> HQ(n) -3.957884e+01 -4.011426e+01 -4.001503e+01 -3.979715e+01

#> SC(n) -3.931154e+01 -3.963312e+01 -3.932005e+01 -3.888833e+01

#> FPE(n) 5.392212e-18 2.729242e-18 2.608833e-18 2.812659e-18

#> 5 6 7 8

#> AIC(n) -4.038139e+01 -4.045602e+01 -4.037132e+01 -4.040225e+01

#> HQ(n) -3.961320e+01 -3.954150e+01 -3.931048e+01 -3.919508e+01

#> SC(n) -3.849054e+01 -3.820500e+01 -3.776014e+01 -3.743090e+01

#> FPE(n) 2.937907e-18 2.750681e-18 3.030708e-18 2.986986e-18

#> 9 10

#> AIC(n) -4.040127e+01 -4.045800e+01

#> HQ(n) -3.904778e+01 -3.895819e+01

#> SC(n) -3.706976e+01 -3.676633e+01

#> FPE(n) 3.054176e-18 2.964556e-18

#>

#>

#> Lag K to use for the VAR Model: 3

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0234304 -0.0053917 0.0003362 0.0059404 0.0227138

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 0.0155410 0.1127942 0.138 0.8906

#> logGNP.l1 1.0329596 0.0981286 10.527 <2e-16 ***

#> rs.l1 -0.2865593 0.1353594 -2.117 0.0363 *

#> rl.l1 0.5689100 0.2728852 2.085 0.0392 *

#> logM1.l2 0.0998010 0.1731782 0.576 0.5655

#> logGNP.l2 0.0347234 0.1317220 0.264 0.7925

#> rs.l2 -0.1180638 0.1842183 -0.641 0.5228

#> rl.l2 -0.4921439 0.3814806 -1.290 0.1995

#> logM1.l3 -0.1859015 0.0999133 -1.861 0.0652 .

#> logGNP.l3 -0.0061578 0.0929415 -0.066 0.9473

#> rs.l3 0.0392050 0.1474719 0.266 0.7908

#> rl.l3 -0.0323000 0.2928387 -0.110 0.9124

#> trend -0.0002258 0.0001064 -2.122 0.0359 *

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008658 on 120 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 8.296e+06 on 13 and 120 DF, p-value: < 2.2e-16

#> Warning: Expected 2 pieces. Missing pieces filled with `NA` in 1 rows [4].

#>

#> Model: AIC Both

#> Trend type: both

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 10 2 2 10

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.982007e+01 -4.053699e+01 -4.057493e+01 -4.052772e+01

#> HQ(n) -3.960059e+01 -4.017118e+01 -4.006280e+01 -3.986926e+01

#> SC(n) -3.927983e+01 -3.963658e+01 -3.931436e+01 -3.890698e+01

#> FPE(n) 5.087308e-18 2.486513e-18 2.399570e-18 2.526125e-18

#> 5 6 7 8

#> AIC(n) -4.047172e+01 -4.050251e+01 -4.042691e+01 -4.048431e+01

#> HQ(n) -3.966695e+01 -3.955141e+01 -3.932949e+01 -3.924056e+01

#> SC(n) -3.849083e+01 -3.816145e+01 -3.772569e+01 -3.742293e+01

#> FPE(n) 2.689264e-18 2.632861e-18 2.877408e-18 2.764981e-18

#> 9 10

#> AIC(n) -4.055474e+01 -4.072060e+01

#> HQ(n) -3.916467e+01 -3.918421e+01

#> SC(n) -3.713319e+01 -3.693889e+01

#> FPE(n) 2.635876e-18 2.297582e-18

#>

#>

#> Lag K to use for the VAR Model: 10

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0215701 -0.0045782 -0.0001255 0.0045321 0.0191265

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 0.0214370 0.1412448 0.152 0.8797

#> logGNP.l1 0.9230416 0.1180599 7.818 1.4e-11 ***

#> rs.l1 -0.0930221 0.1822500 -0.510 0.6111

#> rl.l1 0.2235868 0.3419400 0.654 0.5150

#> logM1.l2 0.3083456 0.2262523 1.363 0.1766

#> logGNP.l2 -0.0372962 0.1599005 -0.233 0.8161

#> rs.l2 -0.1715295 0.2667294 -0.643 0.5219

#> rl.l2 -0.2970080 0.4138644 -0.718 0.4750

#> logM1.l3 -0.5289338 0.2265162 -2.335 0.0219 *

#> logGNP.l3 -0.1303707 0.1543752 -0.845 0.4008

#> rs.l3 0.0821617 0.2954309 0.278 0.7816

#> rl.l3 0.7072648 0.4357963 1.623 0.1084

#> logM1.l4 0.0766561 0.2389938 0.321 0.7492

#> logGNP.l4 0.0795464 0.1565988 0.508 0.6128

#> rs.l4 -0.3737113 0.2945083 -1.269 0.2080

#> rl.l4 -0.3340966 0.4464294 -0.748 0.4563

#> logM1.l5 0.1482905 0.2442165 0.607 0.5453

#> logGNP.l5 0.0972230 0.1565536 0.621 0.5363

#> rs.l5 -0.1840051 0.2871941 -0.641 0.5235

#> rl.l5 -0.2726578 0.4360683 -0.625 0.5335

#> logM1.l6 -0.0045692 0.2447589 -0.019 0.9852

#> logGNP.l6 0.1750043 0.1564919 1.118 0.2666

#> rs.l6 0.2954565 0.2721934 1.085 0.2808

#> rl.l6 -0.1887511 0.4447874 -0.424 0.6724

#> logM1.l7 -0.1346225 0.2397343 -0.562 0.5759

#> logGNP.l7 -0.0089335 0.1563448 -0.057 0.9546

#> rs.l7 -0.3284367 0.2702839 -1.215 0.2277

#> rl.l7 0.1815723 0.4857967 0.374 0.7095

#> logM1.l8 0.2044394 0.2453420 0.833 0.4070

#> logGNP.l8 -0.1242368 0.1569221 -0.792 0.4308

#> rs.l8 0.4117854 0.2765264 1.489 0.1402

#> rl.l8 -0.5335975 0.4859274 -1.098 0.2753

#> logM1.l9 -0.0729486 0.2365466 -0.308 0.7585

#> logGNP.l9 0.0511809 0.1486065 0.344 0.7314

#> rs.l9 0.1154858 0.2439825 0.473 0.6372

#> rl.l9 -0.1193337 0.4895767 -0.244 0.8080

#> logM1.l10 -0.1535998 0.1459102 -1.053 0.2955

#> logGNP.l10 0.0049021 0.1163395 0.042 0.9665

#> rs.l10 0.2452777 0.2004494 1.224 0.2245

#> rl.l10 -0.2537361 0.4113110 -0.617 0.5390

#> const 0.6423768 0.4222415 1.521 0.1319

#> trend 0.0004486 0.0006232 0.720 0.4736

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008479 on 84 degrees of freedom

#> Multiple R-squared: 0.9994, Adjusted R-squared: 0.9991

#> F-statistic: 3276 on 41 and 84 DF, p-value: < 2.2e-16

#>

#>

#> Model: BIC None

#> Trend type: none

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.979949e+01 -4.043610e+01 -4.049031e+01 -4.041841e+01

#> HQ(n) -3.965317e+01 -4.014345e+01 -4.005134e+01 -3.983312e+01

#> SC(n) -3.943933e+01 -3.971577e+01 -3.940982e+01 -3.897776e+01

#> FPE(n) 5.192033e-18 2.748673e-18 2.607880e-18 2.811272e-18

#> 5 6 7 8

#> AIC(n) -4.037845e+01 -4.041713e+01 -4.032619e+01 -4.034898e+01

#> HQ(n) -3.964684e+01 -3.953920e+01 -3.930193e+01 -3.917840e+01

#> SC(n) -3.857764e+01 -3.825616e+01 -3.780505e+01 -3.746768e+01

#> FPE(n) 2.941472e-18 2.852623e-18 3.159796e-18 3.136181e-18

#> 9 10

#> AIC(n) -4.033399e+01 -4.037318e+01

#> HQ(n) -3.901708e+01 -3.890995e+01

#> SC(n) -3.709252e+01 -3.677155e+01

#> FPE(n) 3.247802e-18 3.203453e-18

#>

#>

#> Lag K to use for the VAR Model: 2

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.023513 -0.005879 0.000679 0.005320 0.022638

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 0.08701 0.08370 1.040 0.3006

#> logGNP.l1 1.04867 0.08880 11.810 <2e-16 ***

#> rs.l1 -0.18282 0.12712 -1.438 0.1528

#> rl.l1 0.49240 0.26683 1.845 0.0673 .

#> logM1.l2 -0.10798 0.08225 -1.313 0.1917

#> logGNP.l2 -0.02954 0.08993 -0.328 0.7431

#> rs.l2 -0.17797 0.13646 -1.304 0.1946

#> rl.l2 -0.35810 0.26028 -1.376 0.1713

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008673 on 126 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 1.352e+07 on 8 and 126 DF, p-value: < 2.2e-16

#>

#>

#> Model: BIC Trend

#> Trend type: trend

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.976174e+01 -4.044348e+01 -4.049058e+01 -4.041902e+01

#> HQ(n) -3.957884e+01 -4.011426e+01 -4.001503e+01 -3.979715e+01

#> SC(n) -3.931154e+01 -3.963312e+01 -3.932005e+01 -3.888833e+01

#> FPE(n) 5.392212e-18 2.729242e-18 2.608833e-18 2.812659e-18

#> 5 6 7 8

#> AIC(n) -4.038139e+01 -4.045602e+01 -4.037132e+01 -4.040225e+01

#> HQ(n) -3.961320e+01 -3.954150e+01 -3.931048e+01 -3.919508e+01

#> SC(n) -3.849054e+01 -3.820500e+01 -3.776014e+01 -3.743090e+01

#> FPE(n) 2.937907e-18 2.750681e-18 3.030708e-18 2.986986e-18

#> 9 10

#> AIC(n) -4.040127e+01 -4.045800e+01

#> HQ(n) -3.904778e+01 -3.895819e+01

#> SC(n) -3.706976e+01 -3.676633e+01

#> FPE(n) 3.054176e-18 2.964556e-18

#>

#>

#> Lag K to use for the VAR Model: 2

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0239854 -0.0051696 0.0001681 0.0056556 0.0235511

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 7.899e-02 8.331e-02 0.948 0.345

#> logGNP.l1 1.046e+00 8.825e-02 11.848 <2e-16 ***

#> rs.l1 -2.031e-01 1.269e-01 -1.601 0.112

#> rl.l1 5.214e-01 2.657e-01 1.962 0.052 .

#> logM1.l2 -1.336e-01 8.324e-02 -1.605 0.111

#> logGNP.l2 2.233e-03 9.147e-02 0.024 0.981

#> rs.l2 -2.120e-01 1.372e-01 -1.545 0.125

#> rl.l2 -3.938e-01 2.595e-01 -1.517 0.132

#> trend -1.541e-04 9.498e-05 -1.623 0.107

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008618 on 125 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 1.217e+07 on 9 and 125 DF, p-value: < 2.2e-16

#>

#>

#> Model: BIC Both

#> Trend type: both

#> Seasonality:

#> VARselect Object:

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 10 2 2 10

#>

#> $criteria

#> 1 2 3 4

#> AIC(n) -3.982007e+01 -4.053699e+01 -4.057493e+01 -4.052772e+01

#> HQ(n) -3.960059e+01 -4.017118e+01 -4.006280e+01 -3.986926e+01

#> SC(n) -3.927983e+01 -3.963658e+01 -3.931436e+01 -3.890698e+01

#> FPE(n) 5.087308e-18 2.486513e-18 2.399570e-18 2.526125e-18

#> 5 6 7 8

#> AIC(n) -4.047172e+01 -4.050251e+01 -4.042691e+01 -4.048431e+01

#> HQ(n) -3.966695e+01 -3.955141e+01 -3.932949e+01 -3.924056e+01

#> SC(n) -3.849083e+01 -3.816145e+01 -3.772569e+01 -3.742293e+01

#> FPE(n) 2.689264e-18 2.632861e-18 2.877408e-18 2.764981e-18

#> 9 10

#> AIC(n) -4.055474e+01 -4.072060e+01

#> HQ(n) -3.916467e+01 -3.918421e+01

#> SC(n) -3.713319e+01 -3.693889e+01

#> FPE(n) 2.635876e-18 2.297582e-18

#>

#>

#> Lag K to use for the VAR Model: 2

#> Printing summary of the VAR fit for the variable of interest: logGNP

#>

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0242796 -0.0050814 0.0001488 0.0054701 0.0239546

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logM1.l1 7.934e-02 8.356e-02 0.950 0.3442

#> logGNP.l1 1.045e+00 8.852e-02 11.802 <2e-16 ***

#> rs.l1 -1.804e-01 1.344e-01 -1.342 0.1819

#> rl.l1 4.791e-01 2.782e-01 1.722 0.0875 .

#> logM1.l2 -1.348e-01 8.351e-02 -1.614 0.1090

#> logGNP.l2 -1.170e-02 9.546e-02 -0.123 0.9026

#> rs.l2 -1.989e-01 1.398e-01 -1.423 0.1573

#> rl.l2 -4.136e-01 2.630e-01 -1.573 0.1183

#> const 1.135e-01 2.150e-01 0.528 0.5985

#> trend -2.116e-05 2.693e-04 -0.079 0.9375

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.008643 on 124 degrees of freedom

#> Multiple R-squared: 0.9992, Adjusted R-squared: 0.9991

#> F-statistic: 1.734e+04 on 9 and 124 DF, p-value: < 2.2e-16mdl_build$summarize_build()

#> # A tibble: 10 x 9

#> Model select trend_type season p SigVar OriginalVar Lag MaxLag

#>

#> 1 AIC None aic none 0 3 logGNP~ logGNP -1 -1

#> 2 AIC Tre~ aic trend 0 3 logGNP~ logGNP -1 -1

#> 3 AIC Tre~ aic trend 0 3 rs.l1 rs -1 -1

#> 4 AIC Tre~ aic trend 0 3 rl.l1 rl -1 -1

#> 5 AIC Tre~ aic trend 0 3 trend trend 0 0

#> 6 AIC Both aic both 0 10 logGNP~ logGNP -1 -1

#> 7 AIC Both aic both 0 10 logM1.~ logM1 -3 -3

#> 8 BIC None bic none 0 2 logGNP~ logGNP -1 -1

#> 9 BIC Tre~ bic trend 0 2 logGNP~ logGNP -1 -1

#> 10 BIC Both bic both 0 2 logGNP~ logGNP -1 -1

mdl_build$get_recommendations()

#> # A tibble: 6 x 7

#> Model trend_type season num_sig_vars lag_to_use vars_to_use season_to_use

#>

#> 1 AIC ~ both 0 2 3 logGNP,log~ 0

#> 2 AIC ~ none 0 1 1 logGNP 0

#> 3 AIC ~ trend 0 3 1 logGNP,rs,~ 0

#> 4 BIC ~ both 0 1 1 logGNP 0

#> 5 BIC ~ none 0 1 1 logGNP 0

#> 6 BIC ~ trend 0 1 1 logGNP 0

mdl_build$build_recommended_models()

#>

#> Model: AIC Both - R

#> Trend type: both

#> Seasonality:

#>

#> Printing summary of the VAR fit for the variable of interest: logGNP

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.023681 -0.006032 0.000158 0.006629 0.025152

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logGNP.l1 1.1106065 0.0895101 12.408 <2e-16 ***

#> logM1.l1 0.1854351 0.0807917 2.295 0.0234 *

#> logGNP.l2 -0.0586080 0.1358634 -0.431 0.6669

#> logM1.l2 -0.0559067 0.1432458 -0.390 0.6970

#> logGNP.l3 -0.0881621 0.0886598 -0.994 0.3220

#> logM1.l3 -0.1204991 0.0933103 -1.291 0.1990

#> const 0.2136736 0.1659021 1.288 0.2001

#> trend 0.0002403 0.0002226 1.079 0.2825

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.009169 on 125 degrees of freedom

#> Multiple R-squared: 0.9991, Adjusted R-squared: 0.999

#> F-statistic: 1.932e+04 on 7 and 125 DF, p-value: < 2.2e-16

#>

#>

#> Model: AIC None - R

#> Trend type: none

#> Seasonality:

#> Warning in mdl_build$build_recommended_models(): This recommendation is

#> to use just the variable of interest (dependent variable) to model the

#> time series, hence this model will not be built. Please use a univariate

#> approach to model this separately.

#>

#> Model: AIC Trend - R

#> Trend type: trend

#> Seasonality:

#>

#> Printing summary of the VAR fit for the variable of interest: logGNP

#> Call:

#> lm(formula = y ~ -1 + ., data = datamat)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.0265848 -0.0059894 -0.0002544 0.0059723 0.0253531

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> logGNP.l1 1.001e+00 2.797e-04 3580.480 < 2e-16 ***

#> rs.l1 -3.124e-01 6.648e-02 -4.699 6.51e-06 ***

#> rl.l1 1.678e-01 1.018e-01 1.648 0.102

#> trend 6.039e-05 4.811e-05 1.255 0.212

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.009185 on 131 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 2.427e+07 on 4 and 131 DF, p-value: < 2.2e-16

#>

#>

#> Model: BIC Both - R

#> Trend type: both

#> Seasonality:

#> Warning in mdl_build$build_recommended_models(): This recommendation is

#> to use just the variable of interest (dependent variable) to model the

#> time series, hence this model will not be built. Please use a univariate

#> approach to model this separately.

#>

#> Model: BIC None - R

#> Trend type: none

#> Seasonality:

#> Warning in mdl_build$build_recommended_models(): This recommendation is

#> to use just the variable of interest (dependent variable) to model the

#> time series, hence this model will not be built. Please use a univariate

#> approach to model this separately.

#>

#> Model: BIC Trend - R

#> Trend type: trend

#> Seasonality:

#> Warning in mdl_build$build_recommended_models(): This recommendation is

#> to use just the variable of interest (dependent variable) to model the

#> time series, hence this model will not be built. Please use a univariate

#> approach to model this separately.

# Get only user defined models

# Other options are ony recommended models (subset = 'r') or all models (subset = 'a')

models = mdl_build$get_final_models(subset = 'u')

names(models)

#> [1] "AIC None" "AIC Trend" "AIC Both" "BIC None" "BIC Trend" "BIC Both"

Initialize the ModelCompareMultivariateVAR object

#### With n_step.ahead = TRUE (Default)

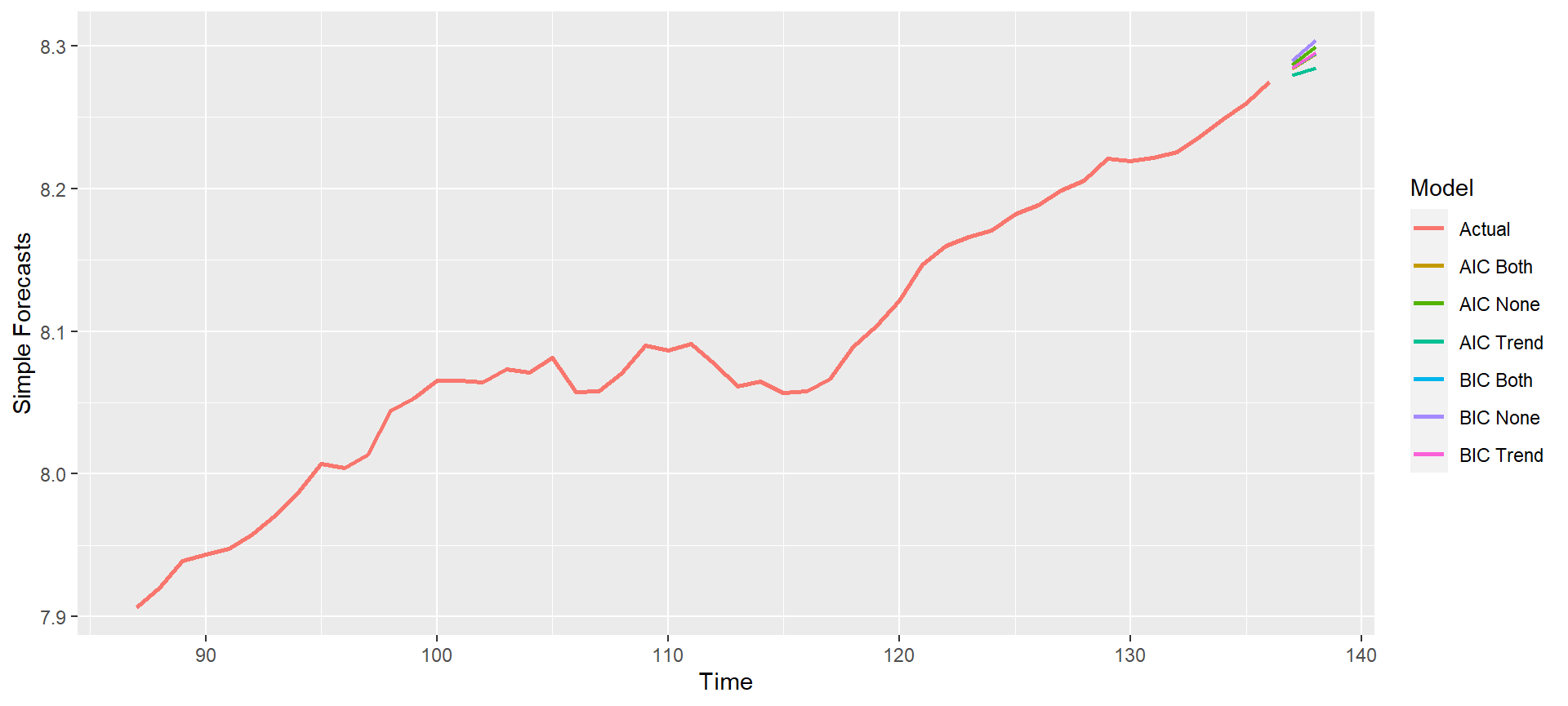

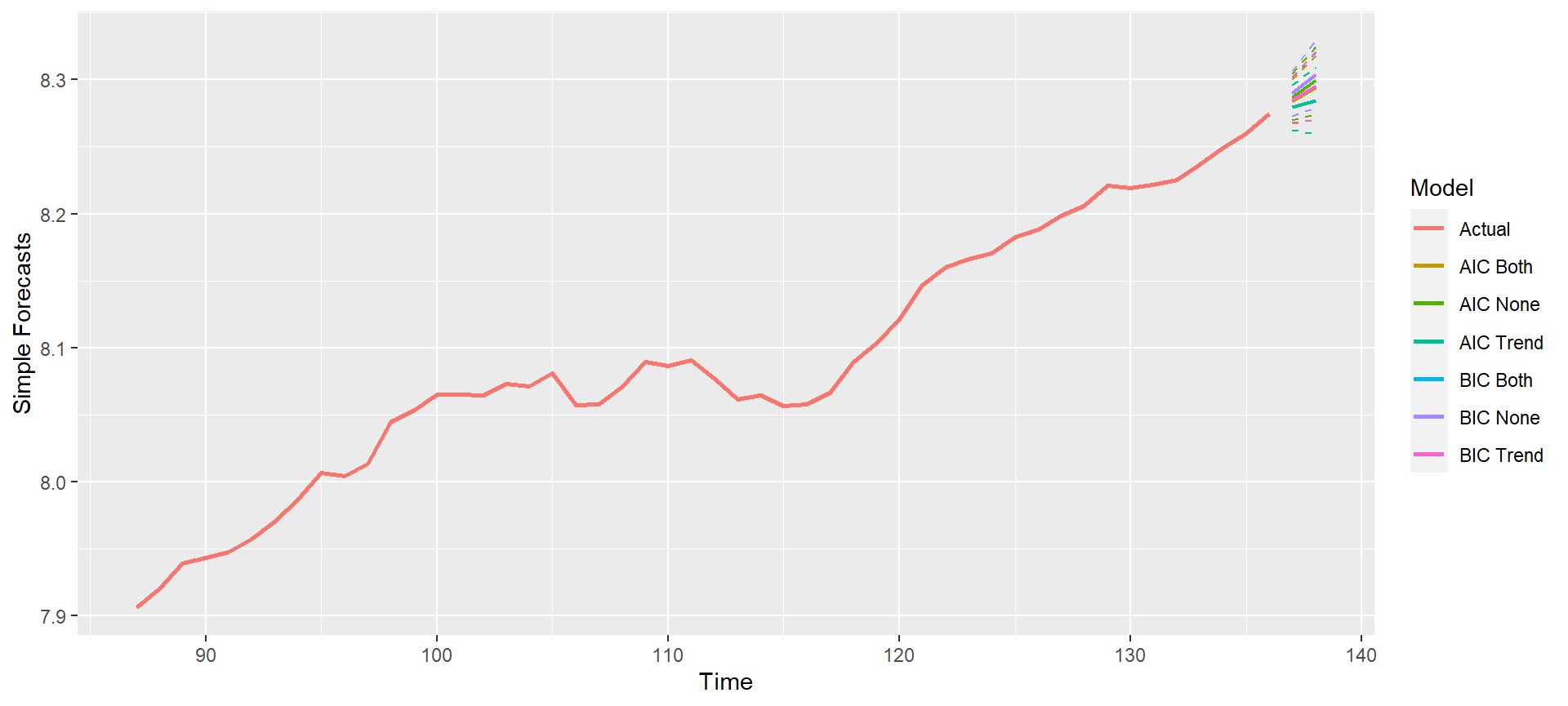

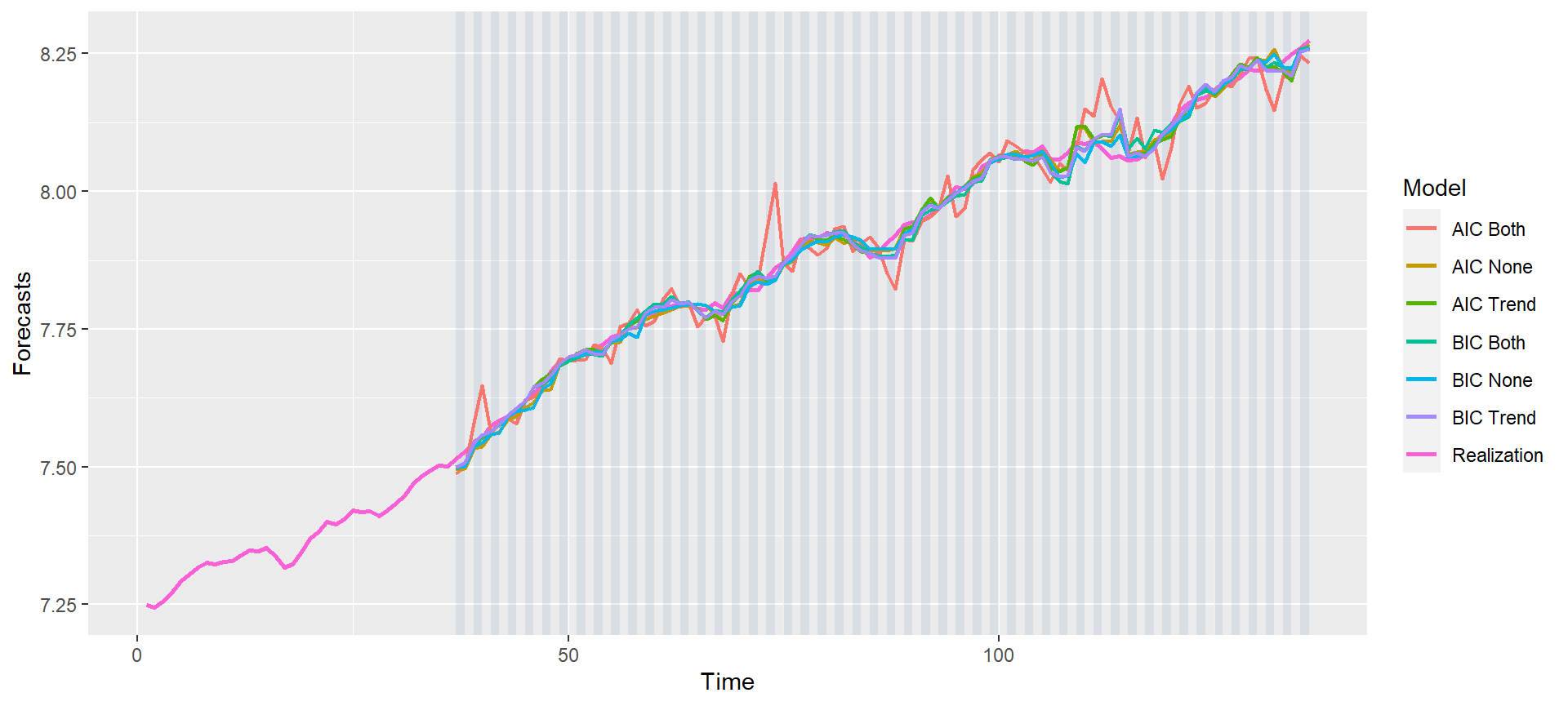

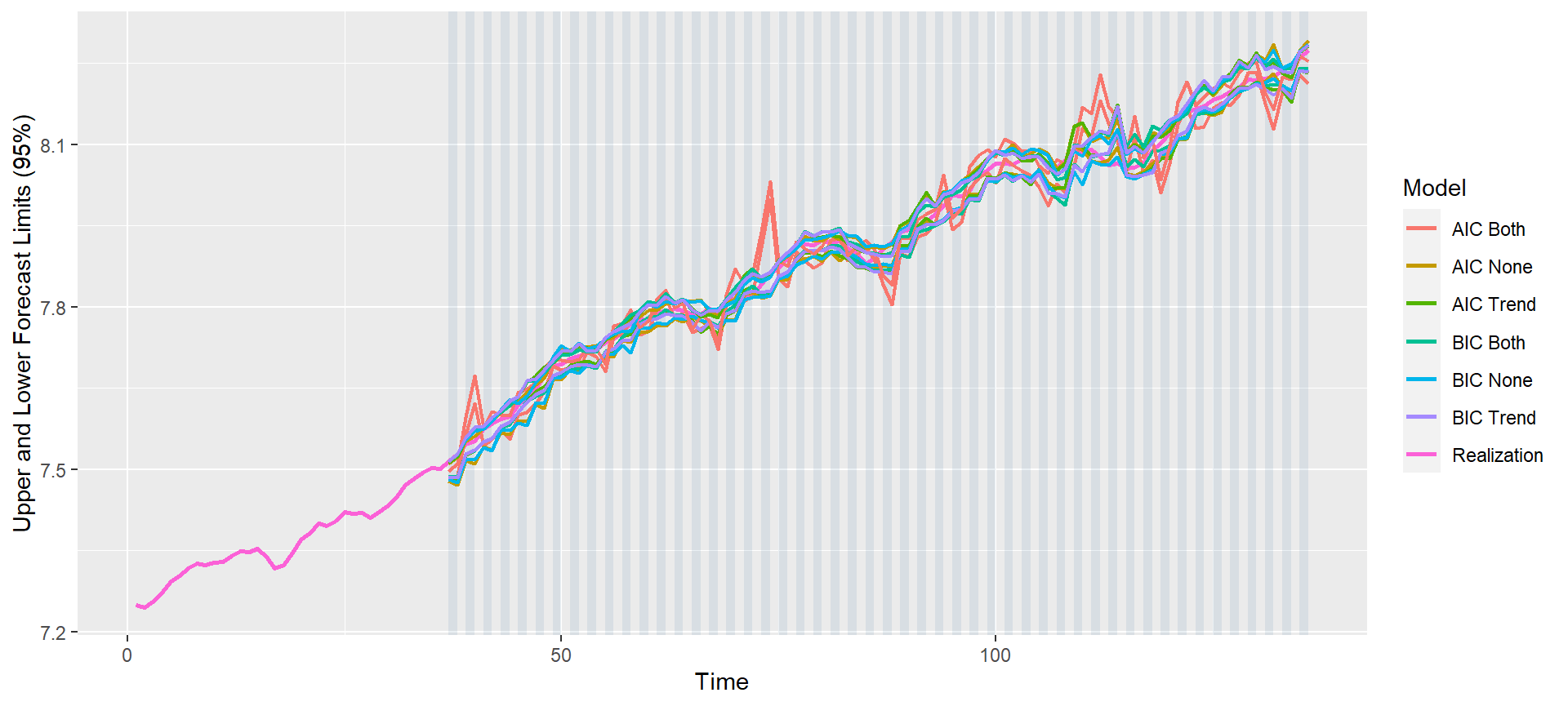

mdl_compare = ModelCompareMultivariateVAR$new(data = data, var_interest = var_interest,

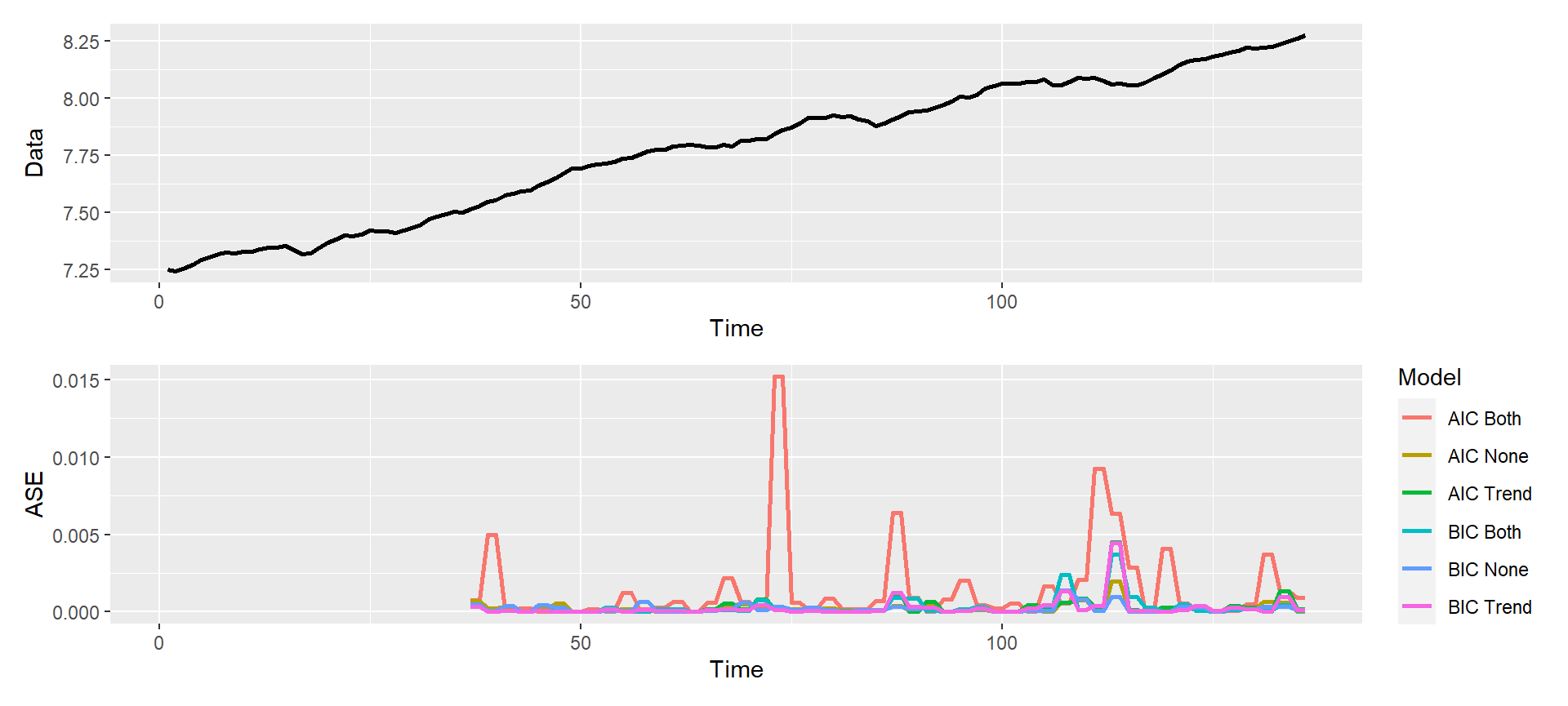

mdl_list = models, n.ahead = n.ahead, batch_size = batch_size, verbose = 1)

#> Warning in private$validate_k(k, batch_size, season = mdl_list[[name]]

#> $varfit$call$season, : Although the lag value k: 10 selected by VARselect

#> will work for your full dataset, is too large for your batch size. Reducing

#> k to allow Batch ASE calculations. New k: 6 If you do not want to reduce

#> the k value, increase the batch size or make sliding_ase = FALSE for this

#> model in the model list

#>

#> Computing metrics for: AIC None

#>

#> Number of batches expected: 50

#> Computing metrics for: AIC Trend

#>

#> Number of batches expected: 50

#> Computing metrics for: AIC Both

#>

#> Number of batches expected: 50

#> Computing metrics for: BIC None

#>

#> Number of batches expected: 50

#> Computing metrics for: BIC Trend

#>

#> Number of batches expected: 50

#> Computing metrics for: BIC Both

#>

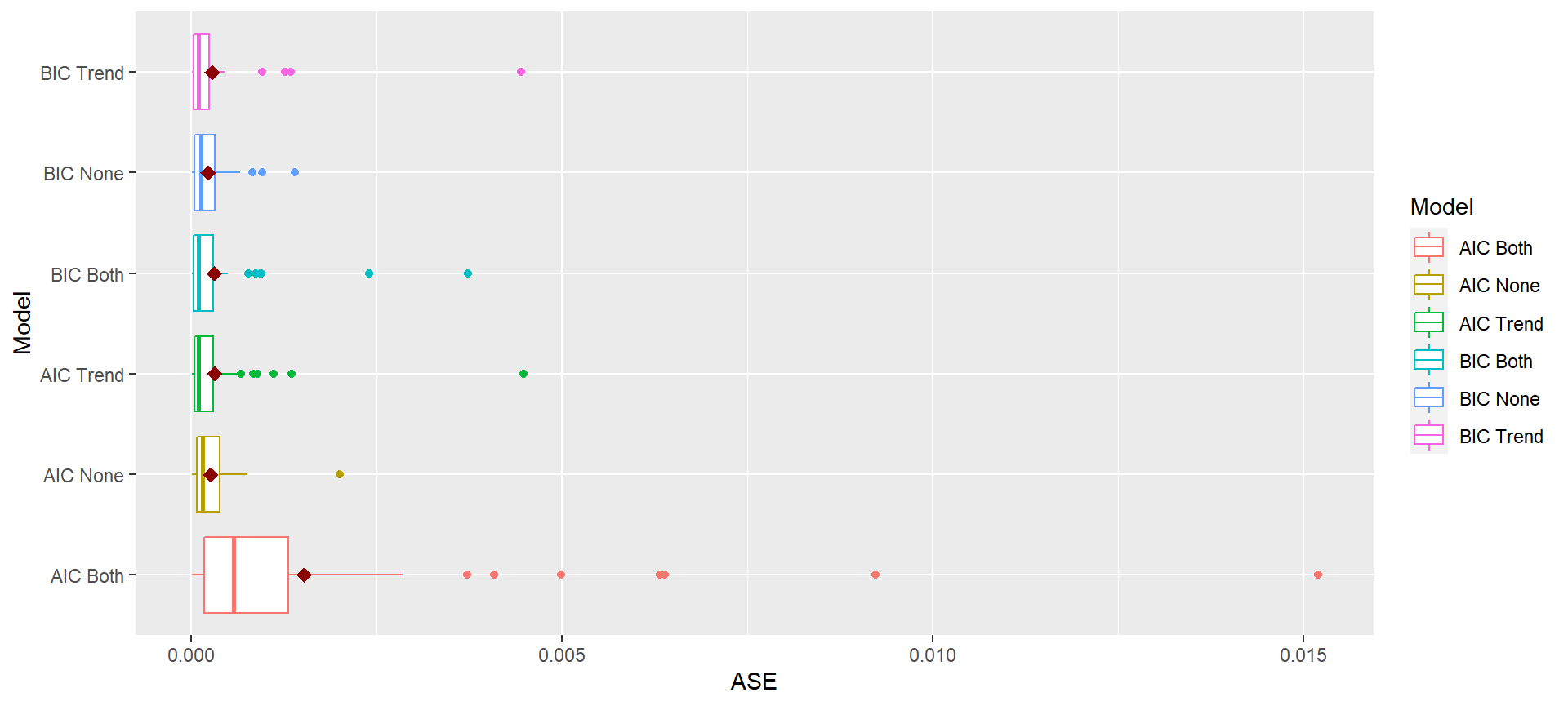

#> Number of batches expected: 50# A tibble: 6 x 6

#> Model Trend Season SlidingASE Init_K Final_K

#>

#> 1 AIC None none 0 TRUE 3 3

#> 2 AIC Trend trend 0 TRUE 3 3

#> 3 AIC Both both 0 TRUE 10 6

#> 4 BIC None none 0 TRUE 2 2

#> 5 BIC Trend trend 0 TRUE 2 2

#> 6 BIC Both both 0 TRUE 2 2